More Related Content

Similar to The OECD-FAO Agricultural Outlook 2024-2033

Similar to The OECD-FAO Agricultural Outlook 2024-2033 (20)

Recently uploaded

Recently uploaded (20)

The OECD-FAO Agricultural Outlook 2024-2033

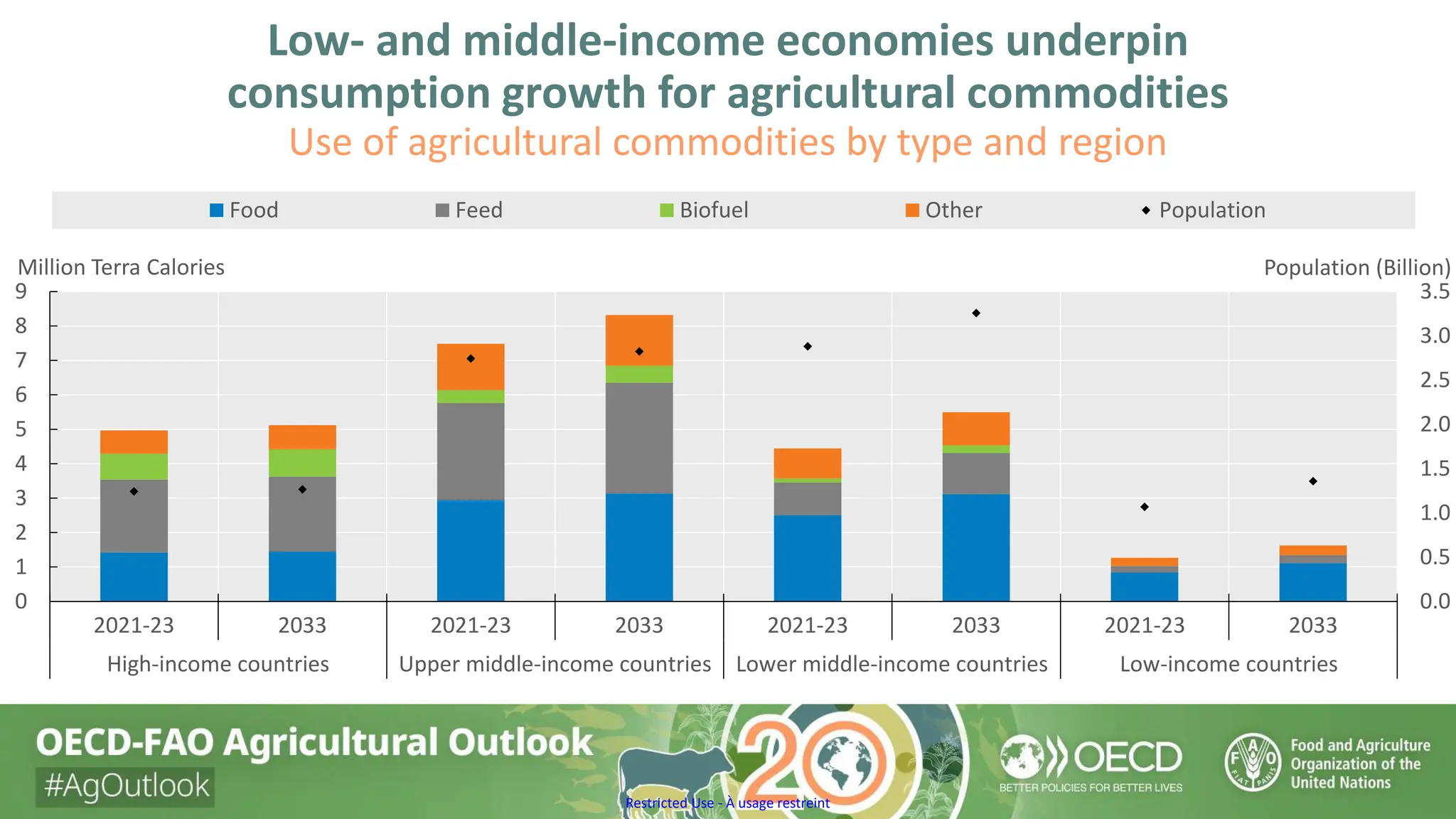

- 1. Restricted Use - À usage restreint Low- and middle-income economies underpin consumption growth for agricultural commodities Use of agricultural commodities by type and region 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 0 1 2 3 4 5 6 7 8 9 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 High-income countries Upper middle-income countries Lower middle-income countries Low-income countries Population (Billion) Million Terra Calories Food Feed Biofuel Other Population

- 2. Restricted Use - À usage restreint Calorie intake is rising but dietary diversification remains slow Contribution of food groups to total daily per capita calorie intake 0 500 1000 1500 2000 2500 3000 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 High-income countries Upper middle-income countries Lower middle-income countries Low-income countries kcal/day/person Staples Animal Products Fats Sweeteners Vegetables & fruits Other MDER (2022)

- 3. Restricted Use - À usage restreint Growing feed use is driven by expansion of herds and increasing intensification of livestock and aquaculture production systems Change in demand for main feed categories 0 50 100 150 200 250 2014-23 2024-33 2014-23 2024-33 2014-23 2024-33 2014-23 2024-33 High-income countries Upper middle-income countries Lower middle-income countries Low-income countries Low protein feed Medium protein feed High protein feed Mt

- 4. Restricted Use - À usage restreint Emerging economies lead the expansion in the use of primary agricultural commodities as feedstocks in biofuels production Share of biofuel and other industrial uses in total use of agricultural commodities 0 10 20 30 40 50 60 70 80 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 Wheat Rice Other coarse grains Maize Sugarcane Vegetable oil Molasses % % of biofuel in total use % of other industrial uses in total use

- 5. Restricted Use - À usage restreint Growth in production continues to be supported mainly by yield gains in low- and middle-income countries Trends in global agricultural production 0 5 10 15 20 25 30 0 100 200 300 400 500 600 700 800 900 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 India China Asia Pacific (excl. China and India) Sub-Saharan Africa Near East and North Africa Europe and Central Asia North America Latin America and the Caribbean % Bln 2014-16 USD Crops Livestock Fisheries Growth in production, 2021-23 to 2033 (right axis)

- 6. Restricted Use - À usage restreint Yield improvements support production growth but there is scope for sustainable intensification Change in projected yields for selected crops and regions, 2021-23 to 2033 0 2 4 6 8 10 12 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 2021-23 2033 Wheat Maize Other coarse grains Rice Soybeans Other Oilseeds Pulses Roots and tubers Developed and East Asia South and Southeast Asia Sub-Saharan Africa Near East and North Africa Europe and Central Asia North America Latin America and Caribbean Global average t/ha

- 7. Restricted Use - À usage restreint Agriculture’s global GHG emissions intensity will decline despite rising emissions in lower and lower-middle income countries GHG emissions and emissions intensity from agriculture, 2021-23 to 2033 Developed and East Asia South and Southeast Asia Sub-Saharan Africa Near East and North Africa Europe and Central Asia Latin America and Caribbean North America -1 -0.5 0 0.5 1 1.5 2 2.5 3 -0.5 0 0.5 1 1.5 2 2.5 3 Annual change in GHG emissions (%) Annual change in production (%)

- 8. Restricted Use - À usage restreint Halving food loss and waste has the potential to reduce global agricultural GHG emissions by 4% and the number of undernourished people by 153 million by the year 2030 Impact on calorie intake and agricultural direct GHG emissions of halving food loss and waste by 2030 -6 -4 -2 0 2 4 6 8 10 12 World High-income countries Upper middle-income countries Lower middle-income countries Low-income countries % Calories Agricultural direct GHG emissions

- 9. Restricted Use - À usage restreint Growth of agricultural trade will slow down and export growth will stabilise Exports as a percentage of production 0 10 20 30 40 50 60 70 Roots and tubers Ethanol Butter Pigmeat Rice Poultry Biodiesel Other oilseeds Cheese Maize Other coarse grains Beef Fish Wheat Cotton Vegetable oils Sugar Soybean Whole milk powder Skim milk powder 2011-13 2021-23 2033 %

- 10. Restricted Use - À usage restreint Prices will resume their long-run trend following 2022 peak Long-term evolution of commodity prices, in real terms 0 50 100 150 200 250 300 350 400 450 500 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018 2021 2024 2027 2030 2033 (2019=100) Soybeans Wheat Maize Beef Pork

Editor's Notes

- Note: the shares are calculated from the data in calories equivalent. The 38 individual countries and 11 regional aggregates in the baseline are classified into the four income groups according to their respective per-capita income in 2018. The applied thresholds are: low: < USD 1 550, lower-middle: < USD 3 895, upper-middle: < USD 13 000, high: > USD 13 000.

- Note: Estimates are based on historical time series from the FAOSTAT Food Balance Sheets database which are extended with the Outlook database. Products not covered in the Outlook are extended by trends. The 38 individual countries and 11 regional aggregates in the baseline are classified into the four income groups according to their respective per-capita income in 2018. The applied thresholds are: low: < USD 1 550, lower-middle: < USD 3 895, upper-middle: < USD 13 000, high: > USD 13 000. Staples include cereals, roots and tubers and pulses. Animal products include meat, dairy products (excluding butter), eggs and fish. Fats include butter and vegetable oil. Sweeteners include sugar and HFCS. The category other includes other crop and animal products. MDER stands for minimum dietary energy requirement

- Note: Low protein feed includes maize, wheat, other coarse grains, rice, cereal brans, beet pulp, molasses, roots and tubers. Medium protein feed includes dried distilled grains, pulses, whey powder. High protein feed includes protein meal, fish meal, and skim milk powder. The 38 individual countries and 11 regional aggregates in the baseline are classified into the four income groups according to their respective per-capita income in 2018. The applied thresholds are: low: < USD 1 550, lower-middle: < USD 3 895, upper-middle: < USD 13 000, high: > USD 13 000.

- Note: Estimates are based on historical time series from the FAOSTAT Value of Agricultural Production domain which are extended with the Outlook database. Remaining products are trend-extended. The net value of production uses own estimates for internal seed and feed use. Values are measured at constant USD of the period 2014-2016.

- Note: Yields are defined as tonnes produced per area harvested. Each symbol represents the average yield for a given commodity within a region. The red lines correspond to the global average per commodity.

- Note: This figure shows projected annual growth in direct GHG emissions from agriculture together with annual growth in the estimated net value of production of crop and livestock commodities covered in the Outlook (measured in constant USD 2014-16 prices). The size of the bubbles corresponds to the level of agricultural GHG emissions in the baseline period 2021-2023. Estimates are based on historical time series from the FAOSTAT Climate Change: Agrifood systems emissions databases which are extended with the Outlook database.CO2 equivalents are calculated using the global warming potential of each gas as reported in the IPCC Sixth Assessment Report (AR6). Emission types that are not related to any Outlook variable (organic soil cultivation and burning savannahs) are kept constant at their latest available value. The category ''other'' includes direct GHG emissions from burning crop residues, burning savanna, crop residues, and cultivation of organic soils. The net value of production uses own estimates for internal seed and feed use.

- Note: Emission estimates are based on historical time series from the FAOSTAT Climate Change: Agrifood systems emissions databases which are extended with the Outlook and Scenario databases. The 38 individual countries and 11 regional aggregates in the baseline are classified into the four income groups according to their respective per-capita income in 2018. The applied thresholds are: low: < USD 1 550, lower-middle: < USD 3 895, upper-middle: < USD 13 000, high: > USD 13 000.

- Note: This share is computed as exports over production (in volume).

- Note: Historical data for soybeans, wheat, maize and beef from World Bank, "World Commodity Price Data" (1960-1989). Historical data for pork from USDA QuickStats (1960-1989).